The Global and Regional Competitiveness Map for 2026

By: Seniors International Consulting (One Health Team)

Introduction

The global macroeconomic scenario in 2026 is defined by a deep interdependence between geopolitical fractures, financial rigidity, and an unprecedented transformation of binding environmental regulations. For strategic advisory firms like Seniors International Consulting, understanding this environment no longer implies analyzing isolated variables, but rather deciphering how volatility in a shipping lane or a regulatory change in Brussels reconfigures balance of payments, investment portfolios, and the commercial viability of value chains in Latin America and the Caribbean

This opinion article analyzes the critical vectors transforming the real economy: the impact of the Middle East crisis, the liftoff of institutional carbon markets, the trade frictions derived from the European Union Deforestation Regulation (EUDR), and the energy transition and green employment strategies defining the Southern Cone's resilience agenda, with special attention to Uruguay's sustainability policies.

1. Global Economic Outlook and the Impact in the Middle East

The conflict in the Middle East has ceased to be a strictly regional hotspot of instability and has consolidated as a catalyst for macroeconomic, financial, and logistical distortions globally.

The Slowdown of Economic Activity and Transmission Channels

Projections from international organizations warn of a sharp deceleration in global growth, which is expected to drop to 2.5% in 2026. This figure stands as the lowest expansion rate recorded since the onset of the COVID-19 pandemic. The slowdown in activity responds to a combination of armed shocks, climate disruptions, and health crises operating through clearly identified channels:

Inflationary and Energy Spiral: Direct damage to extraction and refining infrastructures, combined with operational threats over crucial maritime routes such as the Strait of Hormuz, has steadily increased the cost of oil, liquefied natural gas, and fertilizers.

Logistical and Financial Stress: The partial paralysis of maritime transport corridors forces the rerouting of cargo ships, skyrocketing insurance risk premiums and freight costs. Concurrently, the rise in global sovereign debt and the tightening of monetary policies in advanced economies are making credit more expensive for the emerging block (EMDE), widening financial spreads and limiting the fiscal response capacity of States.

Sanitary, Labor, and Ecological Dimensions

The prolongation of hostilities has shaped a crisis that directly impacts natural capital and the labor fabric:

Ecosystems Under Fire: During the initial weeks of the conflict alone, more than 5 million tons of CO2 were released into the atmosphere due to oil well fires and military operations. Added to this are massive methane leaks and immense crude oil spills in the Persian Gulf that destroy mangroves and collapse the functioning of local desalination plants.

Food and Health Insecurity: The logistical blockage of key components for agricultural inputs raises food prices on a global scale, putting more than 45 million people at risk of acute starvation in net importing nations.

Disruptions in Employment: Industrial paralysis generated by energy volatility creates the risk of a massive labor contraction. At a sector level, various governments have had to enact emergency regulations to govern the consumption of high-demand networks—such as data centers—adapting workforces to an environment of power supply restrictions.

2. Status and Trends of Carbon Pricing

Faced with this adverse global outlook, institutional mechanisms designed to internalize the costs of climate change show unprecedented consolidation, notably led by emerging economies.

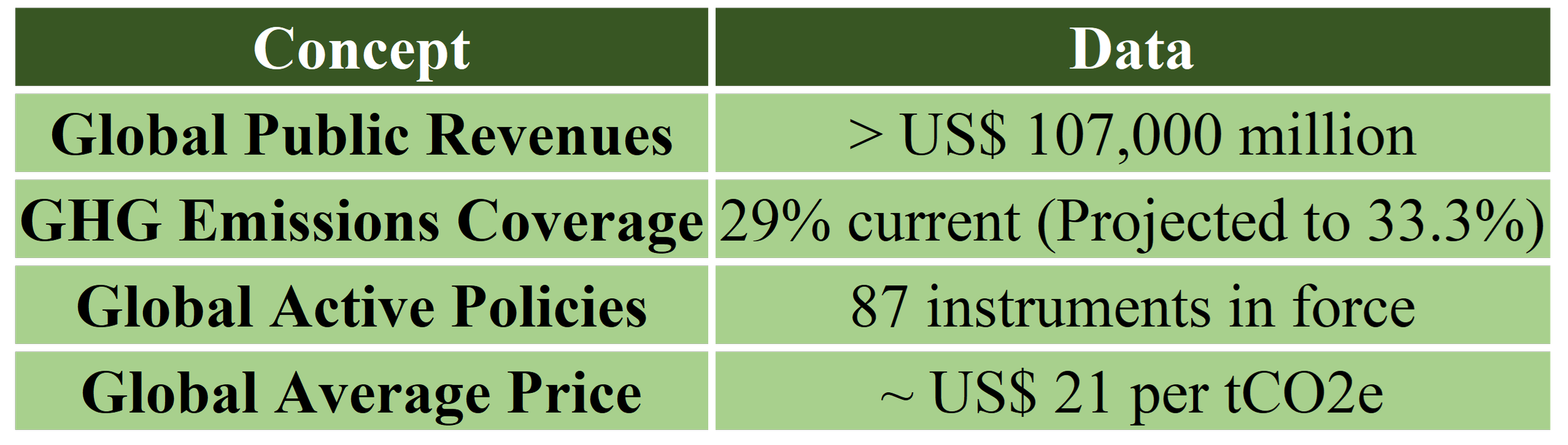

Markets in Figures (2025-2026)

The Cost of Polluting

Historically, greenhouse gas (GHG) emissions operated as an untaxed negative externality; companies polluted without a direct cost and society absorbed the climate impacts. In 2026, this paradigm has changed radically:

Historic Collection: Global public revenues from carbon pricing tripled in the last decade, growing from less than US$ 30,000 million in 2016 to mobilizing more than US$ 107,000 million.

Coverage and Expansion: Currently, 29% of global GHG emissions are covered by direct pricing schemes. Almost a third of the planet's pollution already has an assigned price due to these 87 active policies, divided mainly into two tools: direct carbon taxes and emissions trading systems (pollution quota markets). With the incorporation of instruments under development in middle-income markets—where India and Viet Nam lead implementation—a 33.3% coverage of world pollution is projected.

Market Maturation: The average value per ton of carbon dioxide equivalent (tCO2e) increased by 7%, standing at nearly US$ 21. At the same time, the emission volume of carbon credits grew by 8%, with premium valuations maintained for high-rated projects in forest conservation, reforestation, and international aviation.

3. MERCOSUR-EU Trade Faced with the European Green Deal and the EUDR

The European Union's environmental agenda has ceased to be a declaration of principles to transform into a set of binding trade regulations that exert a critical, restrictive, and transformative impact on regional trade.

The Technical Challenge of the Deforestation Regulation (EUDR)

Following intense political debates, the definitive entry into force of the EU Regulation on deforestation-free products (EUDR) was ratified for December 30, 2026. The rule prohibits the entry into the EU market of soy, beef, wood, rubber, cocoa, and coffee if these goods come from plots deforested after December 31, 2020. The requirement for due diligence forces exporters to trace the origin of each lot using satellite geolocation coordinates.

Sectoral Responses in the Regional Block

The conversion of value chains shows differentiated strategies in the Southern Cone:

Argentina and the VISEC Platform: The Argentine agro-export sector relies on the public-private platform VISEC (Sectoral Vision for Grains and Beef). This tool unifies the individual traceability data of cattle herds with satellite monitoring of sensitive ecoregions such as the Gran Chaco, seeking to prevent lots destined for the EU from mixing with production directed to markets without environmental demands.

Brazil and the Tracking of Indirect Suppliers: Using advanced remote sensing technologies (PRODES/INPE layers), Brazilian soy faces the obstacle of intermediaries in the Cerrado biome. The development of blockchain architectures seeks to ensure that satellite geolocation data accompanies the grain from the originating farm.

Uruguay and Sustainable Differentiation: From an institutional perspective, Uruguay has transformed these requirements into a competitive advantage. The country stands out internationally for consolidating advanced mandatory livestock traceability systems and digital environmental management platforms that allow certifying beef and forestry products as "free from native deforestation" natively and institutionally. This public policy seeks not only to bypass the EU's technical barriers but also to position the country brand under the strictest standards of ecological integrity.

This outlook has sparked formal complaints within MERCOSUR against what is labeled as disguised green protectionism that alters tariff balances. However, the transformative impact is undeniable, acting as a driver for national bioeconomy strategies.

4. Macroeconomic Dynamics in Latin America

In this complex arena, the Latin America and the Caribbean region projects moderate economic growth of 2.2% in 2026(estimating a slight acceleration to 2.5% for the following cycle). However, this evolution is heavily constrained by structural imbalances.

Financial Vulnerability and the Debt Challenge

LAC's macroeconomics evidence a non-linear relationship between debt levels and credit costs. Because a large proportion of countries in the region carry compromised public balances, marginal increases in the debt/GDP ratio trigger severe penalties in sovereign bond spreads. This environment is aggravated by the contagion effect of high interest rates from central banks in advanced economies. The contractionary impact is markedly adverse in energy-importing countries in Central America and the Caribbean, as well as in nations carrying low credit ratings.

Managing Commodity Volatility

The region continues to suffer from chronic fiscal weakness, distinguished by a low accumulation of reserve funds during commodity expansion cycles. Public spending maintains a generalized pro-cyclical behavior: windfall revenues generated by exports immediately expand into current spending instead of being reserved. The World Bank report reveals a deep divergence depending on the type of exporter:

Energy and Metal Exporters: Countries with a mining or oil profile in South America manage to register temporary improvements in their primary balances, although they remain highly exposed to market corrections.

Agricultural Exporters: They represent the highest fiscal risk behavior. They tend to structurally expand current public spending during trade booms, which neutralizes windfall gains and leads to long-term debt accumulation.

5. Energy Transition and Green Employment Strategies in the Region

Faced with the volatility of fossil fuels, the transition toward clean energy matrices is consolidating as the most strategic route to safeguard Latin America's economic sovereignty.

Pillars of Energy Sovereignty

Diversification and Infrastructure: Large-scale investment in solar and wind generation to substitute thermoelectric dependence and protect internal tariffs.

The Green Hydrogen Vector: Development of industrial projects aimed at replacing natural gas in the local production of critical inputs (such as fertilizers), mitigating agri-food vulnerability. On this point, the Uruguayan agenda is advancing firmly through specific state incentives for pilot projects in synthetic fuels and hydrogen derivatives, integrating industrial decarbonization with the attraction of foreign investment.

Storage and Regional Interconnection: Deployment of storage systems and strengthening of cross-border transmission networks to optimize the distribution of clean energy.

The Balance of the Transition Agenda

Absorption of Informal Employment and Investment in Nature

Faced with global warnings indicating that ecological degradation threatens to eliminate the equivalent of 260 million jobs by the year 2050, Nature-based Solutions (NbS) emerge as the primary driver of labor inclusion in the region.

In geographical areas of LAC where rural informality is structural, sustainable agricultural financing is an indispensable tool to anchor local talent. Regenerative agriculture and sustainable forestry programs increase the demand for bio-input specialists and satellite traceability data managers. Likewise, the reconversion toward structured green markets and the removal of trade barriers represent the most efficient channel to reduce the gender gap and formalize rural employment in the regional block.

Conclusion

For a global strategic consulting firm looking from the South to the world, the 2026 landscape forces a redefinition of corporate and institutional priorities. Sustainability has ceased to belong to the sphere of corporate social responsibility to transform into the core of financial resilience and legal viability of international operations.

Strategic advice in the Southern Cone must be structured around three mandatory operational pillars:

Commercial Regulatory Shielding: Conduct due diligence audits and satellite geolocation systems for MERCOSUR exporters, guaranteeing access to the EU market before the December 2026 deadline.

Mitigation of Energy Risks: Design transition strategies and restructuring of energy matrices for large corporations, isolating their production costs from global inflationary shocks.

Human Capital Optimization and ESG Criteria: Structure agricultural financing and labor training programs (upskilling) oriented to green employment, capitalizing on advantageous public traceability infrastructures and institutional regional carbon market schemes.

References

World Bank Group. Global Economic Prospects: Analysis of Emerging Markets, Carbon Pricing, and Agricultural Financing Channels. Washington D.C.: World Bank; May 2026. Report No.: WB-GEP-2026-05.

Sustentabilidad Sin Fronteras. EU-Mercosur Agreement: A Guide on Environmental Rules and the Socioeconomic Impact of the Transition Towards 2026. Buenos Aires: Sustentabilidad Sin Fronteras; January 9, 2026. Available from: https://www.sustentabilidadsinfronteras.org/informes-2026

Sustentabilidad Sin Fronteras. The EU-Mercosur Agreement and the New Requirements of the Deforestation Regulation (EUDR). Buenos Aires: SSF; 2026 [cited 15 Jun 2026]. Available from: https://sustentabilidadsf.org.ar/acuerdo-uemercosur/

Ministry of Environment (Uruguay). Institutional Communications on Sustainability, Green Economy, and Decarbonization Goals in the Uruguayan Productive Sector. Montevideo: Ministry of Environment; 2026 [cited 15 Jun 2026]. Available from: https://www.ambiente.gub.uy/comunicaciones/